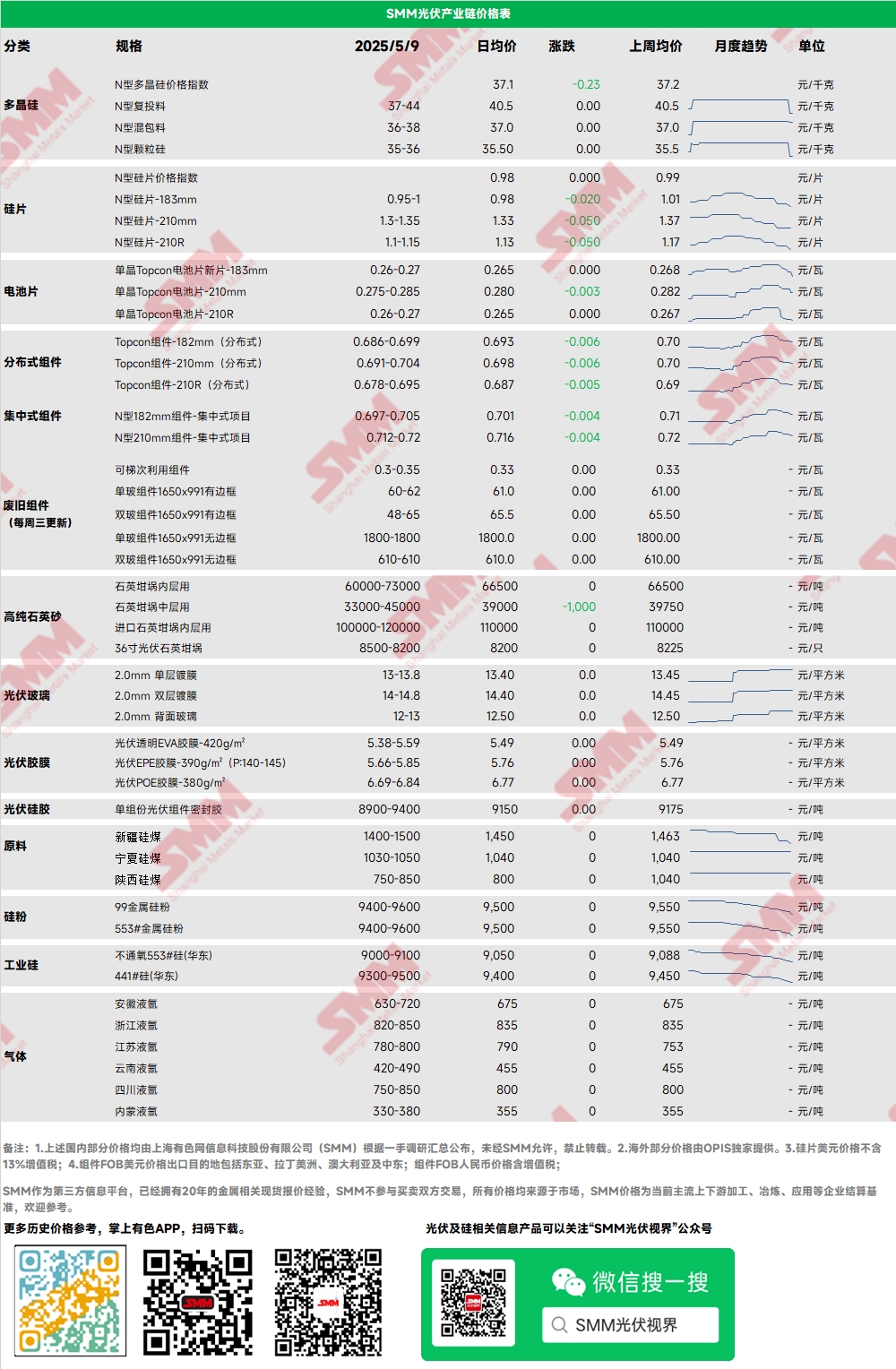

Polysilicon: This week, the mainstream transaction prices for N-type recharging polysilicon in the market ranged from 37 to 44 yuan/kg, with the N-type polysilicon price index at 37.28 yuan/kg. The price center of polysilicon slipped slightly this week, mainly due to weakened market sentiment at the beginning of the week. Subsequently, as the futures market collapsed, market sentiment was further impacted. Top-tier enterprises began to show signs of standing firm on quotes to support the market, with some halting quotations. The concentrated trading period after the Labour Day holiday has passed, and market transactions have been limited, with most maintaining a wait-and-see attitude.

Wafer: This week, the prices for domestic N-type 18Xmm wafers ranged from 0.95 to 1.05 yuan/piece, with N-type 210R wafers priced at 1.15 to 1.2 yuan/piece and N-type 210mm wafers at 1.35 to 1.4 yuan/piece. Overall market sentiment was poor, with downstream purchase demand remaining flat. The price of 183mm wafers fell again, with individual prices reaching as low as 0.95 yuan/piece. Market transactions were moderate during the Labour Day holiday, with top-tier enterprises maintaining orders at 1 yuan/piece. After the holiday, as downstream market conditions weakened, the wafer market followed suit with price declines. The latest production schedule for wafers in May is approximately 55GW+, representing a decrease compared to April MoM.

Cell: For P-type cells, the mainstream quotation for 182P was 0.29-0.295 yuan/W, with a significant contraction in overall demand scale. For N-type cells, quotations for 183N ranged from 0.26-0.27 yuan/W, 210RN from 0.26-0.27 yuan/W, and 210N from 0.275-0.285 yuan/W. Among these, prices for 210RN and 183N have fallen the fastest recently, reaching the lowest point for the entire year of 2024. There are two main reasons for this: firstly, the continuous decline in upstream wafer prices has driven down cell costs; secondly, the shrinking of end-use demand has led to an increase in industry inventory levels, motivating solar cell plants to reduce prices to boost shipments. Currently, the market is observing the future trend of wafer prices, with module producers showing low purchase willingness and testing the downward elasticity near the 0.26 yuan/W price point. Some top-tier cell producers are still adhering to a strategy of standing firm on quotes. If wafer prices have reached the bottom, cell price reductions would cause revenue to fall below the cost line; if wafer prices continue to decline, there is room for cell prices to fall further.

Module: This week, the price of PV modules accelerated its downward trend. The mainstream transaction price for N-type 182mm modules in centralized projects ranged from 0.7-0.71 yuan/W, with the average price decreasing by 0.006 yuan/W. The mainstream transaction price for N-type 210mm modules ranged from 0.715-0.725 yuan/W, with the average price decreasing by 0.009 yuan/W. The price of distributed N-type 182 modules was around 0.693-0.705 yuan/W, with the average price decreasing by 0.011 yuan/W compared to last Friday. The price of distributed N-type 210 modules was 0.698-0.71 yuan/W, with the average price decreasing by 0.011 yuan/W compared to last Friday. The price of distributed N-type 210R modules was 0.683-0.7 yuan/W, with the average price decreasing by 0.015 yuan/W compared to last Friday.This week, the inversion between distributed and centralized PV module prices persisted, with prices for some orders scheduled for delivery in May-June already falling below 0.65 yuan/W (including freight), and forward order prices approaching previous lows. According to SMM, the average winning bid price for the 26.667 GW module centralised procurement order of China National Nuclear Corporation (CNNC) was 0.686 yuan/W, with a delivery date of March 31, 2026. These prices are comparable to the forward module prices, indicating that the terminal market is relatively optimistic about demand in the second half of this year and Q1 next year, sending a positive signal to the market.

Terminal: From April 28, 2025, to May 4, 2025, SMM recorded a total of 23 awarded project sections for PV modules involving multiple enterprises, including CSI Solar Co., Ltd., Jinko Solar Co., Ltd., and Hunan Redsolar New Energy Technology Co., Ltd., with 12 projects disclosing installed capacities. The main types of PV modules procured and awarded this week were N-type. The winning bid prices for PV modules were concentrated in the range of 0.66-0.85 yuan/W, with a weekly weighted average price of 0.75 yuan/W, an increase of 0.06 yuan/W compared to last week. As all awarded projects this week were small-scale, the winning bid prices were relatively high, resulting in a 0.06 yuan/W increase in the weekly weighted average price. The total procurement capacity for awarded projects this week was 43.33 MW, a decrease of 927.59 MW compared to last week. Due to the coincidence of the end of April and the Labour Day holiday this week, the total procurement capacity for awarded projects was significantly affected by the timing. The clearly identified procurement capacity for N-type modules this week was approximately 39.98 MW, accounting for 92.29%.

Film: This week, the price of PV-grade EVA ranged from 11,000 to 11,700 yuan/mt. Demand for foaming-grade and cable-grade EVA slowed down, leading to a significant price decline. In May, new order prices for film in the demand side decreased, and the narrowing price spread forced the raw material side to offer discounts, slowing down the transaction pace in the EVA market. Overall, transactions were average, and film enterprises maintained a wait-and-see attitude. It is expected that EVA prices will continue to be under pressure.

The mainstream price range for EVA film was 13,000-13,200 yuan/mt, and the price range for EPE film was 14,500-15,000 yuan/mt, with prices declining. On the demand side, module prices fell, and demand weakened. On the cost side, the price of PV-grade EVA pulled back, providing cost support for the decline in film prices.

The domestic delivery-to-factory price of POE remained stable at 12,000-14,000 yuan/mt. Although some petrochemical enterprises were still in the maintenance period, under the dual pressures of gradually weakening demand and the gradual release of new capacity, it is expected that the price of PV-grade POE will be under pressure.

PV glass: This week, the price center of some PV glass enterprises remained stable. As of now, the mainstream quotation for 2.0mm single-layer coated PV glass in China was 13.5 yuan/m², with some enterprises reducing their quotations to 13 yuan/m². The mainstream quotation for 3.2mm single-layer coated PV glass was 22.0 yuan/m², and the mainstream quotation for 2.0mm back-sheet glass was 12.0 yuan/m².This week, domestic module enterprises have yet to commence procurement activities, focusing instead on inquiries, negotiations, and price suppression. Glass enterprises have seen a slight increase in their glass inventory. Affected by the decline in module prices, there is strong resistance among module enterprises towards glass procurement. Given the current profit margins for glass, enterprises have appropriately reduced their quotations, adopting a volume discount strategy. It is expected that the center of trading prices will continue to move downward in the future.

High-purity quartz sand: This week, some domestic high-purity quartz sand products have seen a slight decrease in quotations. The current market quotations are as follows: inner-layer sand is priced at 60,000-73,000 yuan/mt, middle-layer sand at 33,000-45,000 yuan/mt, and outer-layer sand at 18,000-25,000 yuan/mt. Domestic wafer prices continued to decline this week. Amid the overall weak market performance, the trading volume of quartz sand has also rapidly decreased. Some enterprises that previously increased their quotations have now started to reduce them. The center of mainstream market quotations has shifted downward by approximately 2,000 yuan/mt. It is anticipated that, under the combined influence of weakening demand and narrowing downstream profits, quartz sand prices will remain in the doldrums.

》Check the SMM PV Industry Chain Database

![[SMM PV News] Armenia Hits 1.1 GW Solar Capacity,](https://imgqn.smm.cn/usercenter/qQwIB20251217171741.jpg)

![Spot Market and Domestic Inventory Brief Review (February 5, 2026) [SMM Silver Market Weekly Review]](https://imgqn.smm.cn/usercenter/tSwaX20251217171735.jpg)